Anatomy of a Buydown: Temp’ 2-1 vs. Fixed (& a simple test that holds up)

A challenging market to time a refinance, source: https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed

I’ve been talking with a lot of builders. Incentives are everywhere. They’re not identical across the country. Many differ between communities of the same builder. Alas, the common thread is the 2-1 buydown.

If you’re new to the term, a temporary buydown is a payment subsidy not below market interest rate. Most lenders require the cost o the buy down to be funded by the seller or builder. Your payment is calculated “as if” the interest rate were 2 percentage points lower in year 1 and 1 point lower in year 2. Despite the payment relief, the loan still accrues interest and amortizes at the note rate. Variations exist (1-0, 1-1), but 2-1 is the most common. The concept of the buy down has been used before, and was as prominent in the mortgage market twenty years ago.

Since 2-1s are still active in Q4 2025, it made sense to back-test them against the rate improvement we’ve seen over the past year. The question: in a falling-but-choppy rate market, is a temporary buydown better than a permanent buydown, and when is the time to refi?

Dates & Data

The 30-year fixed has bounced around the 6.25 to 7.25 percent range over the past twelve months. Using the Mortgage News Daily index, I anchored two rates roughly a year apart and about 0.90 percentage point apart. The purpose is to set up the effective buydown to use for short term purposes and enough time and rate improvement to consider refinancing.

7.51% on Apr 30, 2024 [retest of the 2 year high]

6.60% on Apr 4, 2025 (about 11 months later, @ 90 bps lower)

Useful context from the same source:

24-month recent peak: 7.58% on Nov 13, 2023

24-month recent low: 6.11% on Sep 17, 2024

Source: Mortgage News Daily, 30-year fixed [https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed]

Assumptions & Parameters

For a clean illustration and for easy comparison,

Loan amount: $100,000 after down payment and closing costs

Term: 30 years

Close date: Apr 30, 2024

No taxes, insurance, or MI included in the math

Option 1: Temporary 2-1 buydown at a 7.51% note

Year 1 payment calculated as if 5.51%

Year 2 payment calculated as if 6.51%

Builder subsidy dollars that fund the payment gap:

Year 1: $1,575.72

Year 2: $803.62

Total: $2,379.34

The $2,379.34 is a builder charge at signing. These funds are transferred to an escrow account where its doled out monthly based on the effective rate for year 1 and 2. If you payoff early, the balance should be credited to your loan payoff. Note, the loan still amortizes at 7.51%.

Option 2: Permanent buydown to 6.99%

Assume the builder will apply equal buydown costs, roughly 2.3 points of builder credit to secure 6.99% for the full 30 years. In real pricing, 1 point usually buys about 0.25% lower in rate. Getting to a full half-point can be a stretch, but this is a fair working assumption for today’s illustration.

Option 3: Refi the Buy-Down Loan after 12 months

As a foil, a refinance opportunity presents itself, 90bps lower that the original note rate of 7.51%, nearly 12 months later…

Refi at month 12 to 6.60%

Roll $2,000 in hard fees into the new balance

Apply the entire unused year-2 buydown escrow ($803.62) as a payoff credit at refi

New term 29 years so the total timeline still equals 30 years

This keeps the amortization comparison fair and shows that amortization always follows the note rate, not the temporary “as-if” rate.

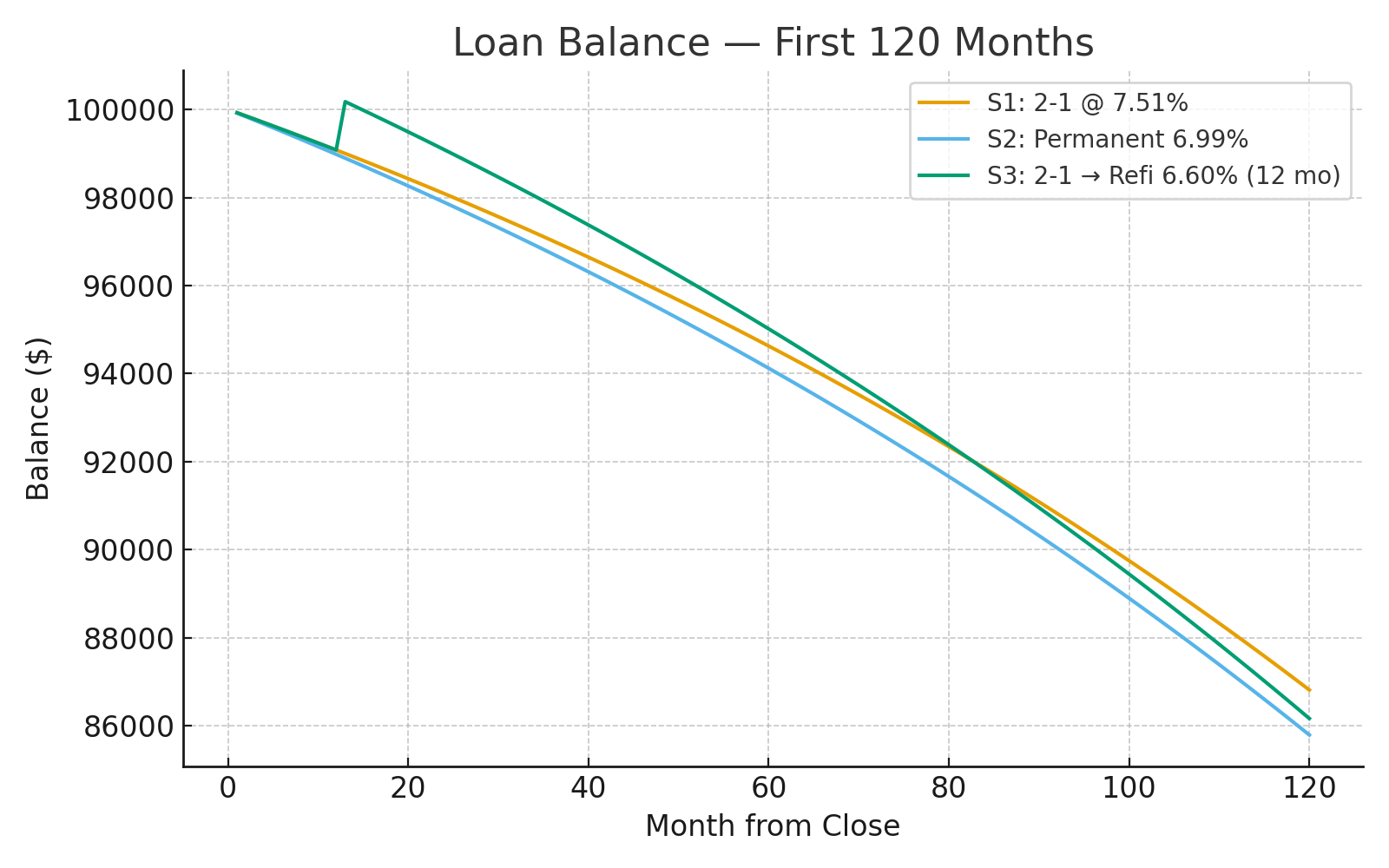

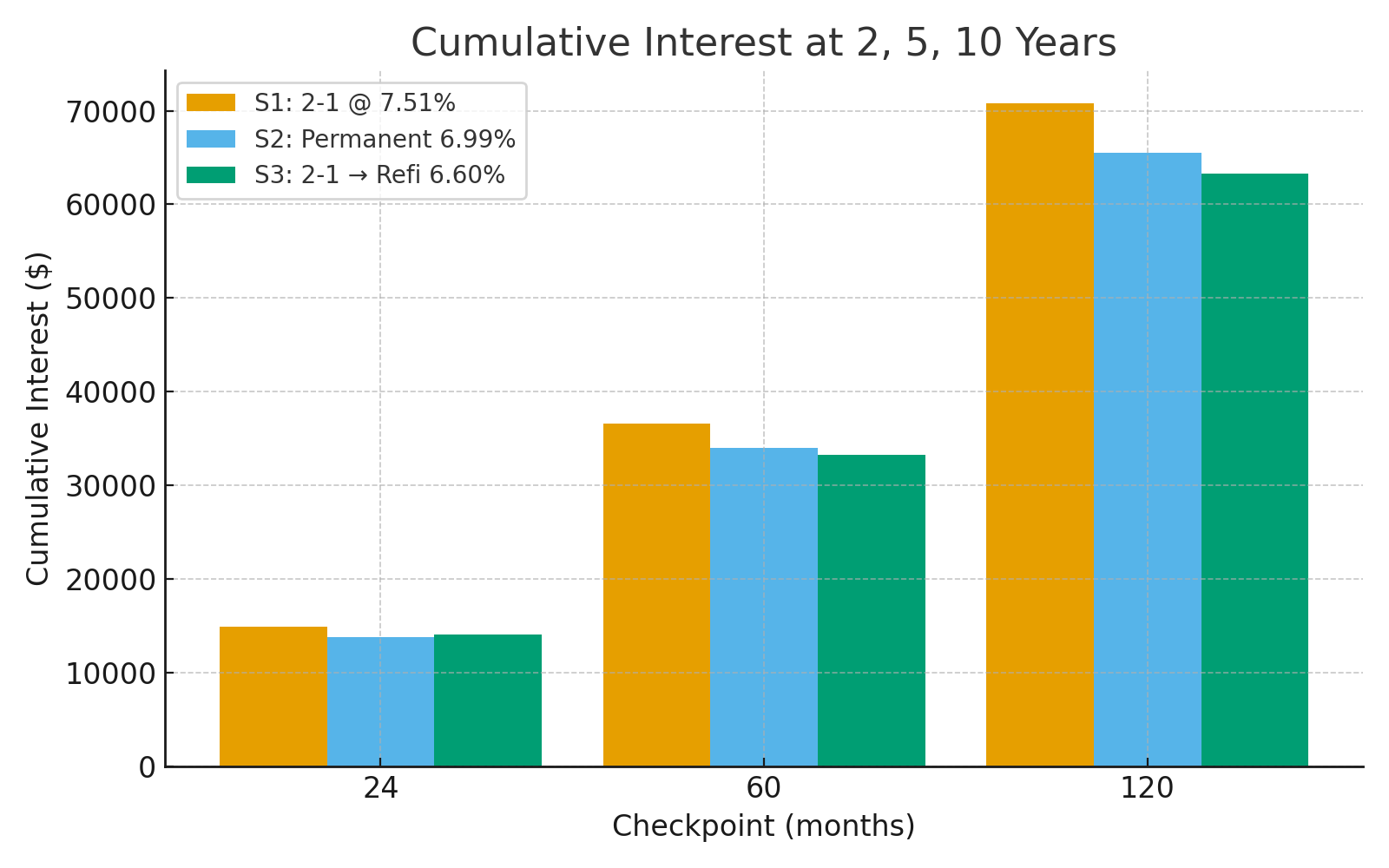

Results: Balances, Equity, & Interest

A reasonable way to compare the loans is where are are on the amortization years after. Using round figures at the 2, 5, and 10-year marks from the original close:

After 2 years

Balance: 2-1 $98.0k | Permanent $97.3k | Refi $98.8k

Equity: 2-1 $2.0k | Permanent $2.7k | Refi $1.2k

Cumulative interest: Permanent 6.99% is lower than Temp 2-1 Buydown. Refi sits close to 2-1 at 2 years because the first 12 months still accrue at 7.51% before the refi.

After 5 years

Balance: 2-1 ≈ $94.6k | Permanent ≈ $93.7k | Refi ≈ $95.3k

Equity: 2-1 ≈ $5.4k | Permanent ≈ $6.3k | Refi ≈ $4.7k

Cumulative interest: Best to worst = Permanent, Refi, 2-1.

After 10 years

Balance: 2-1 ≈ $86.2k | Permanent ≈ $84.8k | Refi ≈ $85.6k

Equity: 2-1 ≈ $13.8k | Permanent ≈ $15.2k | Refi ≈ $14.4k

Cumulative interest: Best to worst = Permanent, Refi, 2-1.

What the back-test tells…

The 2-1 feels great on payment in year 1 and still good in year 2. However, the permanent 6.99% still comes out ahead in this example. It delivers lower interest and more equity at every interval, 2, 5, and 10 years. It costs money, or equity to refinance and proves that slow and steady wins out..

The 2-1 + refi to 6.60% finishes second. You get genuine year-one relief, the benefit of a payoff credit from the unused escrow, and a better note via refinance. The downside is the first 12 months at 7.51% are baked in, and financing $2,000 in fees blunts some of the gain on a $100k balance. There is very little principal paid in the first years.

Last, the 2-1 with no refi trails because once the subsidy ends you are back at 7.51% for the long haul.

Q4 update: rates 0.25% better than the refi target

If the refi lands near 6.35% instead of 6.60%, that can help. On a $100k loan it’s still modest. It narrows the gap versus the 6.99% permanent but usually does not flip the result over 5 to 10 years because you already paid a year at 7.51% and you financed refi costs.

Where a 0.25% improvement can matter: larger balances and files where the unused buydown escrow is sizeable relative to the balance at month 12. That can push the refi path ahead sooner.

Rule of thumb from this back-test: to beat a 6.99% permanent with a 2-1 then refi, you typically want a refi rate at least 0.50% to 0.75% lower than 6.99% and you want it early enough for compounding to work. 6.60% gets close, 6.35% gets closer, but neither clearly beats a permanent 6.99% at $100k over the mid-term. At $300k to $600k, the math leans more toward the refi as the dollars scale.

Practical Guidance

The 2-1 buydown is a payment tool, not a rate change. Amortization always follows the note rate. During the buydown you are not paying down principal faster and you are not reducing interest accrual versus the note rate. The monthly payment is being subsidized but the amortization stays the same. Knowing that the length of the buydown is only two years suggest that you should start to look at refinancing as soon as the math says so. That can be fine if you can land a meaningfully better rate soon, but it is a plan, not a given.

Matty’s recommendation,

If you expect to hold the loan 5 years or longer and the builder will fund the equivalent buy down costs in points, run the math. In this example, the permanent 6.99% wins for both equity and total interest.

If you prefer payment relief use the 2-1, but plan a refi only if you can realistically improve the rate by at least 0.25% or more, reduce the payment by a minimum of $100 per month on this size loan, and recover closing costs inside 12 - 18 months.

Do not let subsidy dollars go stale. Get a written incentive menu showing temporary buydown, permanent points, and closing-cost credits. Allocate the credit where it does the most good for your timeline. Also confirm in writing that any unused buydown escrow will credit to payoff at refi.

Illustration only. Excludes taxes, insurance, and MI. Rate availability and pricing vary by day, market, and file quality. Source for rate anchors: Mortgage News Daily.