Borrow Buy Build Blog

Fixed Price vs Cost Plus in Custom Construction [the difference and clear choice?]

Found the lot? Choose the right contract, fixed price vs cost-plus, for your custom home.

If you’re building a custom home, the two main worries are how much and how long. Your answers depend much on your organization with the builder and lender you choose, and the contract you sign. While there is no universal contract for a custom home build, most buyers face two paths. A fixed-price contract, where the builder commits to a lump sum for a defined scope. Or a variable-price (cost-plus) contract, where you pay actual costs for labor and materials plus a builder fee. Both work really well. Since the pandemic, most deals I see have shifted toward cost-plus. The right choice comes down to how complete your plans are, how much flexibility you want, and how much risk you’re willing to own.

What a Fixed Price contract really means

A fixed price contract is straightforward. You and the builder agree on a number for a specific set of plans and specifications. If the builder runs into material price increases or longer lead times, that risks rests on the builder, not you, as long as the scope does not change.

For example, the “Martin family” is building a 3,200 square foot home on a on a subdivided lot. They have owned the parcel for years giving them the time they need to have complete plans, a detail spec sheet including selections for cabinets, counters, flooring, lighting, and appliances. Their builder prices the job at a fixed number and includes allowances that match their selections. During the build, the Martins decide to change nothing. As their lender orders inspections, the draw schedule ties to clear milestones. Friction is low, fundings are predictable, and the final cost breakdown matches dollar for dollar with the contract.

The trap with fixed price is a budget filled with estimates. If the contract says “solid surface counters” without brand and level, and defined cost, that can leave you exposed. If the lighting allowance covers builder grade materials but your selections live a tier higher, that gap lands on you. You can protect yourself by insisting on a detailed costs sheet that lists brand, color, and model notes for key materials. If the contract includes an escalation clause, push for a cap and a defined index that triggers it.

What a Variable Price contract really means

Variable price contracts value flexibility. You pay actual job costs plus an agreed upon fee. This structure favors evolving plans or a builder that can supply subs with that prioritize delivery time or by costs. Sometimes this set up can save money, time, or both versus a fixed number. The tradeoff for the flexibility is increased risk. If cabinets costs increase, you own the difference. It may require you to reduce part of your budget on another line item. We witnessed a lot of this during the pandemic, which reminds us controls matter.

Consider my clients the Jinerks. They want a customized kitchen with glass railings, and a feature stair they will design during framing. They picked a cost-plus contract with a transparent fee and weekly cost reports. The builder agrees to targets in big categories like cabinetry, tile, and glazing. Any cost above the threshold requires a written approval. When the stair design comes in 150% more than they anticipated, they pivoted by downgrading the front door design. This was they were able to stay within the budget without adding a cost overrun. The project stays honest because the reporting is tight and they understand how to pivot.

Cost-plus goes sideways when the budget is soft, approvals are lax, or when materials are not ordered in accordance to timeline. If you choose variable pricing, demand line item budgets, actual vendor bids for major trades, a clear fee structure, and weekly job cost reports that show original budget, committed amounts, and remaining to complete. Set approval thresholds in writing so everyone knows when a choice needs a signature. Require two or three bids on large trades unless you document a sole source reason.

How the Contract changes the Closing

Signing your custom home contract? Compare fixed price vs cost-plus before you sign

The one thing I remind all of my clients building is that once you sign your loan papers, its not possible to increase the loan amount. Cost increases are okay and normal, but the responsibility is all yours. Prior to the pandemic most contracts were for a fixed price. Lenders prefer a clean sheet. Fixed price is usually easier to underwrite because the signed contract lines up with complete plans and a makes the appraisal a number they can match. Draws are timely and predictable. Title updates and inspections are simpler.

Cost-plus becomes a problem as lenders list to see a contingency line item. Some lenders like to pad the figures with a flat 10% to add to the budget. While there is no right or wrong number for the contingency that number should be between you and your builder. There is no reason to add a 10% contingency on top of a variable priced contract IF the contract already calls for a 10% contingency. Yet, we see many lenders struggle with what is sufficient to mitigate the risks of cost overruns. Adding the extra contingency can complicate your qualifying by increasing the amount of capital your loan needs to close and the value your appraisal needs to meet.

Typically, the greater the loan amount, the greater the downpayment. If the appraisal comes in lower than the outlined costs then you may need a loan that allows for a higher loan-to-value or more down payment at closing. It is difficult to modify the budget to adjust to the appraisal and get the lender to approach the same application with a second appraisal. It happens, even in this market, and there are always solutions. Partnering with a lender that offers some flexibility in LTV, a set contingency or reserve requirements can alleviate any appraisal deficiencies.

What to expect next, 2026?

You do not need an analyst to plan well. It comes down to an honest conversation with your builder, your lender, and adequate timelines. Do not rush the process and use all the time you need before you break ground.

Rates have eased from the peak but still range bound in the 6 percent range. A twelve-month build can live along or against interest rate cycles. Lenders like to price interest rates according to the time of construction. Larger timelines will usually increase the interest rate offered. If your builder’s schedule says ten months, set your rate plan around that, not around hope. Having a float down before your loan converts to permanent financing can help tremendously.

Materials costs remain higher, but volatility is not gone. Lumber, window packages and custom cabinets can still shift. Fixed price shifts more of that risk to the builder if your spec is tight and the escalation clause is capped. Cost-plus can handle change better if you set caps in big categories and take competing bids on large trades.

Most builders I meet with tell me that labor remains tight. Protect schedule with realistic durations and a builder who shows current capacity in writing. If a subcontractor backlog is the critical path, put that date on the calendar and connect on it weekly.

Ask your contractor about their process of who is responsible for permits and lead time. New energy codes lift HVAC and input costs. Research insurance requirements for the builders risk and permanent policy. Some carriers have had a difficult time writing insurance due to fire risks or coverage limitations. Build those realities into the budget before you sign.

Prospective buyer viewing a house under construction, researching contract types for 2026.

The Proper Contract?

If your know exactly what you wish to build and your site is straightforward, a fixed price is still the cleanest way to execute. You gain payment certainty and fewer draw edits. The price may include a builder’s volatility premium, but you get a calm build.

If you want the freedom to adjust during construction, and have the time and liquidity, a cost-plus can work well. Besides the time and money it will require discipline. You need weekly a clear outline on any change orders and targets for the big categories. Set a realistic contingency and protect it from casual use. When you treat cost-plus like a fixed budget that you can change on purpose, not by accident, you get the flexibility you want without losing the project to drift.

Famous Last Words

Finding a buildable lot and at a reasonable price remains a challenge. For many of my clients, building a home is a lifelong goal, a decision that is not impacted by the cost of a mortgage. As budgets shift, execution and a lender’s creativity matter more than headlines. Both fixed-price and variable-price contracts can work right now and into 2026. Pick the structure that matches how you make decisions, then back it up with a plan that is clearly organized. Identify your material specs, a draw schedule tied to realistic milestones, a builder approved contingency, with a single close loan that allows for a float down at delivery. That’s how you keep your custom home on budget and your stress in check.

Anatomy of a Buydown: Temp’ 2-1 vs. Fixed (& a simple test that holds up)

A challenging market to time a refinance, source: https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed

I’ve been talking with a lot of builders. Incentives are everywhere. They’re not identical across the country. Many differ between communities of the same builder. Alas, the common thread is the 2-1 buydown.

If you’re new to the term, a temporary buydown is a payment subsidy not below market interest rate. Most lenders require the cost o the buy down to be funded by the seller or builder. Your payment is calculated “as if” the interest rate were 2 percentage points lower in year 1 and 1 point lower in year 2. Despite the payment relief, the loan still accrues interest and amortizes at the note rate. Variations exist (1-0, 1-1), but 2-1 is the most common. The concept of the buy down has been used before, and was as prominent in the mortgage market twenty years ago.

Since 2-1s are still active in Q4 2025, it made sense to back-test them against the rate improvement we’ve seen over the past year. The question: in a falling-but-choppy rate market, is a temporary buydown better than a permanent buydown, and when is the time to refi?

Dates & Data

The 30-year fixed has bounced around the 6.25 to 7.25 percent range over the past twelve months. Using the Mortgage News Daily index, I anchored two rates roughly a year apart and about 0.90 percentage point apart. The purpose is to set up the effective buydown to use for short term purposes and enough time and rate improvement to consider refinancing.

7.51% on Apr 30, 2024 [retest of the 2 year high]

6.60% on Apr 4, 2025 (about 11 months later, @ 90 bps lower)

Useful context from the same source:

24-month recent peak: 7.58% on Nov 13, 2023

24-month recent low: 6.11% on Sep 17, 2024

Source: Mortgage News Daily, 30-year fixed [https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed]

Assumptions & Parameters

For a clean illustration and for easy comparison,

Loan amount: $100,000 after down payment and closing costs

Term: 30 years

Close date: Apr 30, 2024

No taxes, insurance, or MI included in the math

Option 1: Temporary 2-1 buydown at a 7.51% note

Year 1 payment calculated as if 5.51%

Year 2 payment calculated as if 6.51%

Builder subsidy dollars that fund the payment gap:

Year 1: $1,575.72

Year 2: $803.62

Total: $2,379.34

The $2,379.34 is a builder charge at signing. These funds are transferred to an escrow account where its doled out monthly based on the effective rate for year 1 and 2. If you payoff early, the balance should be credited to your loan payoff. Note, the loan still amortizes at 7.51%.

Option 2: Permanent buydown to 6.99%

Assume the builder will apply equal buydown costs, roughly 2.3 points of builder credit to secure 6.99% for the full 30 years. In real pricing, 1 point usually buys about 0.25% lower in rate. Getting to a full half-point can be a stretch, but this is a fair working assumption for today’s illustration.

Option 3: Refi the Buy-Down Loan after 12 months

As a foil, a refinance opportunity presents itself, 90bps lower that the original note rate of 7.51%, nearly 12 months later…

Refi at month 12 to 6.60%

Roll $2,000 in hard fees into the new balance

Apply the entire unused year-2 buydown escrow ($803.62) as a payoff credit at refi

New term 29 years so the total timeline still equals 30 years

This keeps the amortization comparison fair and shows that amortization always follows the note rate, not the temporary “as-if” rate.

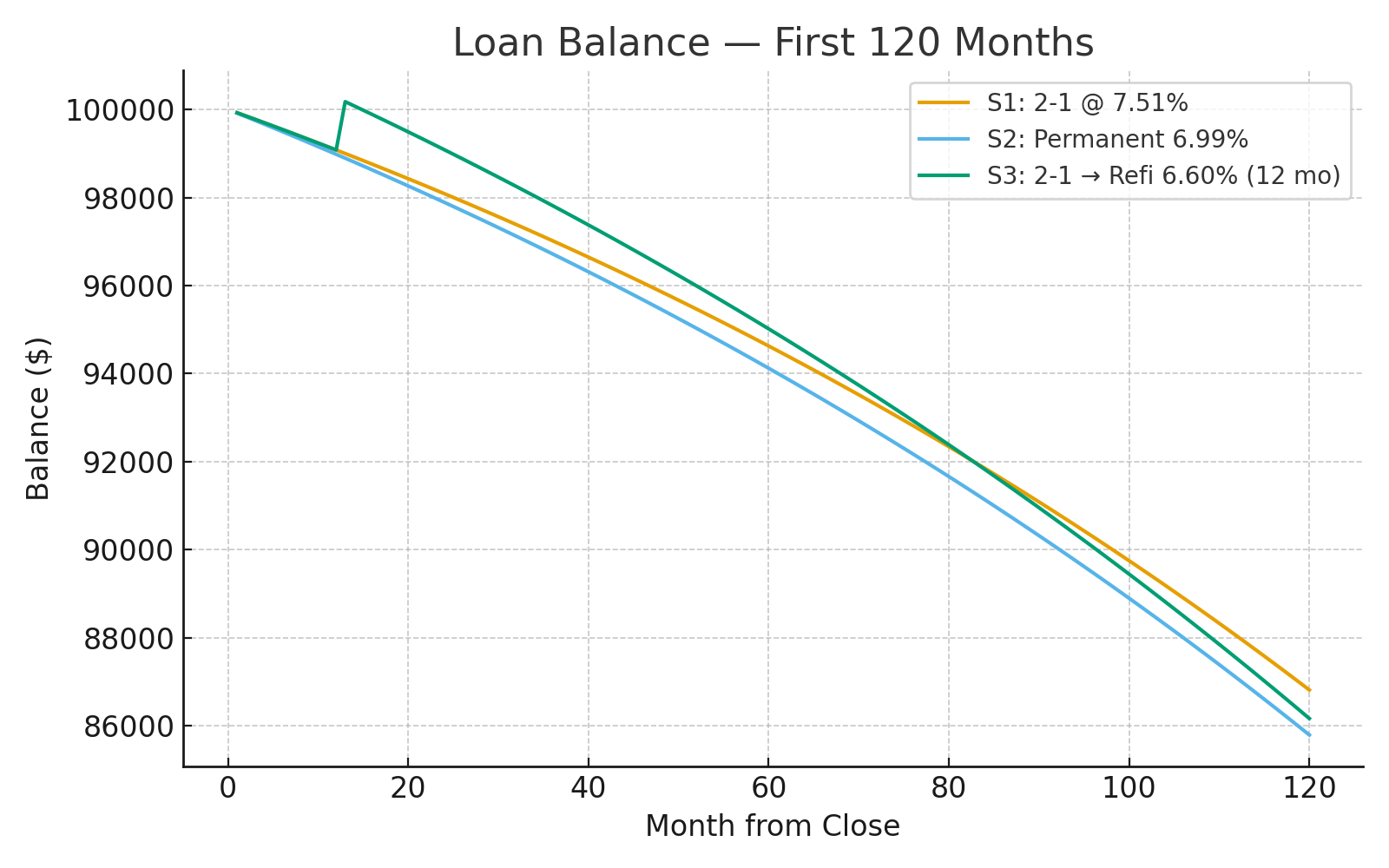

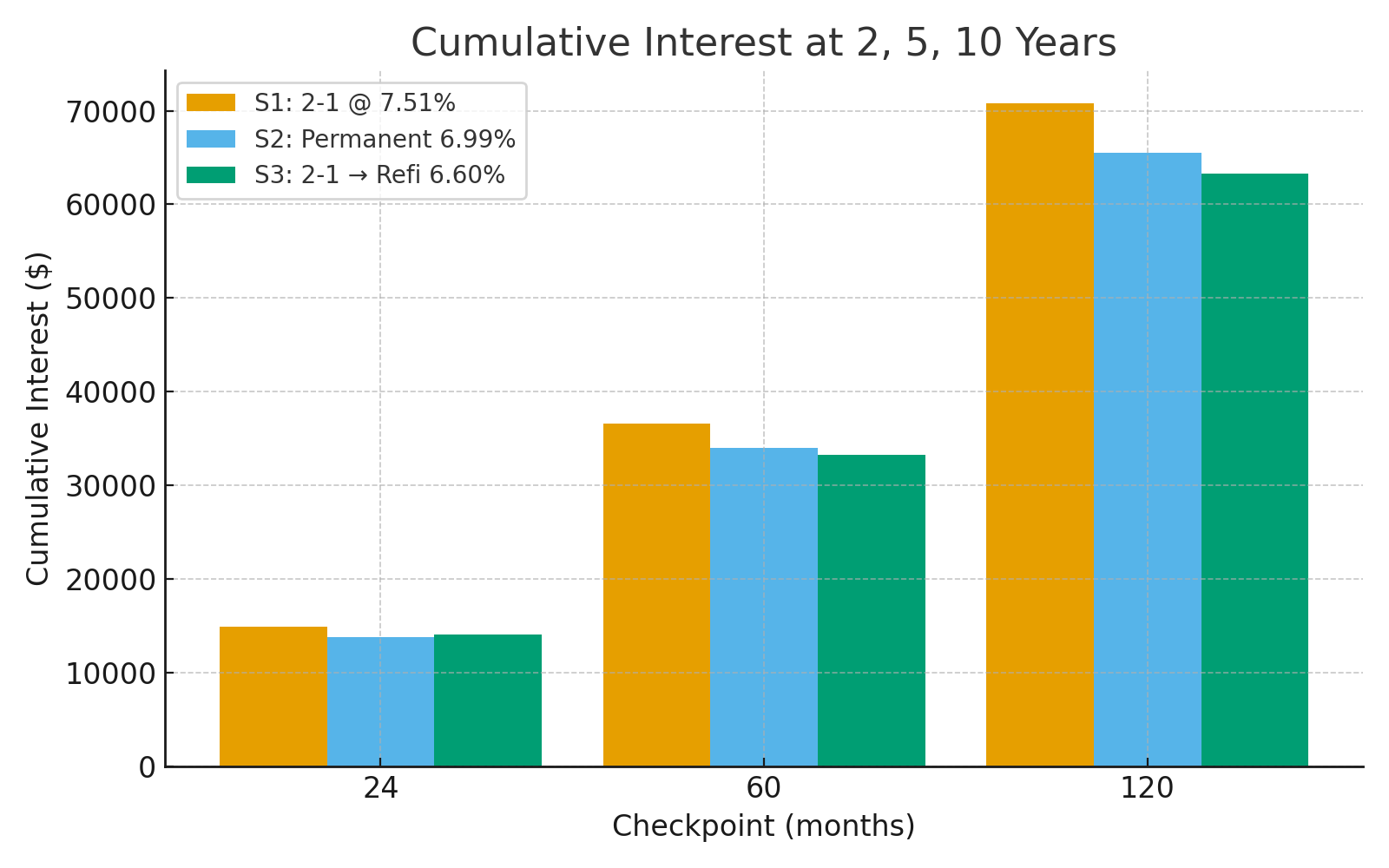

Results: Balances, Equity, & Interest

A reasonable way to compare the loans is where are are on the amortization years after. Using round figures at the 2, 5, and 10-year marks from the original close:

After 2 years

Balance: 2-1 $98.0k | Permanent $97.3k | Refi $98.8k

Equity: 2-1 $2.0k | Permanent $2.7k | Refi $1.2k

Cumulative interest: Permanent 6.99% is lower than Temp 2-1 Buydown. Refi sits close to 2-1 at 2 years because the first 12 months still accrue at 7.51% before the refi.

After 5 years

Balance: 2-1 ≈ $94.6k | Permanent ≈ $93.7k | Refi ≈ $95.3k

Equity: 2-1 ≈ $5.4k | Permanent ≈ $6.3k | Refi ≈ $4.7k

Cumulative interest: Best to worst = Permanent, Refi, 2-1.

After 10 years

Balance: 2-1 ≈ $86.2k | Permanent ≈ $84.8k | Refi ≈ $85.6k

Equity: 2-1 ≈ $13.8k | Permanent ≈ $15.2k | Refi ≈ $14.4k

Cumulative interest: Best to worst = Permanent, Refi, 2-1.

What the back-test tells…

The 2-1 feels great on payment in year 1 and still good in year 2. However, the permanent 6.99% still comes out ahead in this example. It delivers lower interest and more equity at every interval, 2, 5, and 10 years. It costs money, or equity to refinance and proves that slow and steady wins out..

The 2-1 + refi to 6.60% finishes second. You get genuine year-one relief, the benefit of a payoff credit from the unused escrow, and a better note via refinance. The downside is the first 12 months at 7.51% are baked in, and financing $2,000 in fees blunts some of the gain on a $100k balance. There is very little principal paid in the first years.

Last, the 2-1 with no refi trails because once the subsidy ends you are back at 7.51% for the long haul.

Q4 update: rates 0.25% better than the refi target

If the refi lands near 6.35% instead of 6.60%, that can help. On a $100k loan it’s still modest. It narrows the gap versus the 6.99% permanent but usually does not flip the result over 5 to 10 years because you already paid a year at 7.51% and you financed refi costs.

Where a 0.25% improvement can matter: larger balances and files where the unused buydown escrow is sizeable relative to the balance at month 12. That can push the refi path ahead sooner.

Rule of thumb from this back-test: to beat a 6.99% permanent with a 2-1 then refi, you typically want a refi rate at least 0.50% to 0.75% lower than 6.99% and you want it early enough for compounding to work. 6.60% gets close, 6.35% gets closer, but neither clearly beats a permanent 6.99% at $100k over the mid-term. At $300k to $600k, the math leans more toward the refi as the dollars scale.

Practical Guidance

The 2-1 buydown is a payment tool, not a rate change. Amortization always follows the note rate. During the buydown you are not paying down principal faster and you are not reducing interest accrual versus the note rate. The monthly payment is being subsidized but the amortization stays the same. Knowing that the length of the buydown is only two years suggest that you should start to look at refinancing as soon as the math says so. That can be fine if you can land a meaningfully better rate soon, but it is a plan, not a given.

Matty’s recommendation,

If you expect to hold the loan 5 years or longer and the builder will fund the equivalent buy down costs in points, run the math. In this example, the permanent 6.99% wins for both equity and total interest.

If you prefer payment relief use the 2-1, but plan a refi only if you can realistically improve the rate by at least 0.25% or more, reduce the payment by a minimum of $100 per month on this size loan, and recover closing costs inside 12 - 18 months.

Do not let subsidy dollars go stale. Get a written incentive menu showing temporary buydown, permanent points, and closing-cost credits. Allocate the credit where it does the most good for your timeline. Also confirm in writing that any unused buydown escrow will credit to payoff at refi.

Illustration only. Excludes taxes, insurance, and MI. Rate availability and pricing vary by day, market, and file quality. Source for rate anchors: Mortgage News Daily.

Buying New Construction Now: Why This Could Be The Turn

Over the past year, new homes have gone from “for sale” to “on sale.” If you are new home shopping there is a lot to appreciate; improving interest rates, more inventory and choices. While that is good news in any market, incentives on new homes are piling up. Builders are telling me that things are still selling despite less foot traffic than last summer. It does not add up, but the National Association of Home Builders reports that builder confidence is rising. Real estate is a proposition that favors sellers the majority of the time and the last time we saw a glimpse of a buyers market was 10 years ago. While we are not yet in a buyers market for resale, the new segment is ripe. A brand new home with a discounted price with a below market rate can only last so long.

Year Over Year Changes

It is easy to point to the affordability issue and conclude wages have a lot of ground to make up still. Despite the probability of revisions to the home home sales number for August, it was unexpected. While future expectations are encouraging, increased activity curtesy of lower rates, the current index of 37 is more telling. A year ago October the reading was 43, but today rates are better and that overlap has to end sometime. We’re below the 50, as the ‘neutral’ line, which is why incentives are still strong. That’s your edge if you move now.

Oct 2025: 37, with future sales expectations 54 and buyer traffic 25.

Oct 2024: 43, with future sales expectations 57 and traffic 29. [1]

While mortgage rates are considered elevated, they have improved. Payments are improving before you add in builder concessions and buydowns.

30-year fixed average: 6.19% October, 2025,

30-year fixed average 6.54% October 2024.[2]

Today the Fed hosts meeting 9 of 10. One more cut is expected in December. Here is a snapshot of short term rates which help Home Equity Lines and some Adjustable Rate mortgage.

Fed funds

Now: 4.00% to 4.25% after the Sep 17, 2025 cut.

Then: 4.75% to 5.00% after the Sep 18, 2024 cut. [3]

Prime rate

Now: 7.25% (effective Sep 18, 2025).

Then: 8.00% (effective Sep 19, 2024).[4]

A bigger surprise is the supply of new home inventory as reported by the Census. This could be why future confidence is rising.

Latest: 7.4 months of supply in Aug 2025.

For perspective, here is a snapshot of the resale market and inventory time. Buyers have some strength in the market, but no where near the command in the new home segment. The net effect is that with more resale homes on the market, the concentration of new homes have some down a few percentage points. Currently new homes make up 26.8% of the market. [6]

Inventory up 14% year over year with a median marketing time of 33 days

Home supply is 4.6 months [7]

Time to send in the Wolf (Street) and ask pretty please, “Are More Price Cuts Coming?”

Wolf Street has touched on the theme the whole year. Builders are relying on incentives, showing the effective prices slipped more than contract prices. Further, completed home inventory matched the highest level we have seen since August 2009. [8] In speaking with new home sales teams, there are healthy discounts on models and specs, but not cuts across the board. With resale and new home market experiencing higher levels of inventory, there’s plenty room for negotiating.

Buy Now, or Wait and See?

Short answer, new construction is way more buyer friendly. NAHB’s study in October shows 65% of builders using incentives, 38% cutting prices, making the average cut 6%. It’s a wait and see game for builders as rates trickle down, they will not need to buydown rates. Builders are still moving a units despite the headwinds, so I expect the season of giving to end sometime by next year. [9]

Survey says rates matter the most, just ask 78% of all home builders. Today we will see another quarter-point discount from the Fed and the odds are for one more in December. The economy is slowing which should help prices and should encourage more buyers to step up. This is a market where the buyers do not buy price, they buy payment. Hence, the most often asked question this year remains “do you offer a 40 year loan?”

Take the market for what it is, a mix of incentives and price reductions. The affordability factor will increase over time but I would not sleep on how quickly the incentive market will change.

Shop this market, like a boss

Pay attention to the data. Try to stay on top of marketing times and inventory. Pay attention to new communities that have recently opened and the incentives and how you can take advantage of every dollar. Two weeks ago I was at a community that was brand new and they were offering 50% off upgrades and $20k to use towards costs and buydowns. It was a fabulous deal.

Use long term rate locks with float downs. Its built in rate insurance, so if rates hang around or do the unthinkable, you stay protected. But if they trend down, and you can pick up a lower rate for free, it’s the cherry on top. New construction is always a moving target, so confirm your rate lock is beyond your estimated close date. Last, make sure you compare rate quotes apples to apples as some lender collect a deposit that is non-refundable. Others add a premium to the current market rate and cap the float down.

Compare resale to new construction. It’s more than a sticker price conversation. New homes win with their warranty and maintenance costs in the first few years. However, we have noticed lately many of new homes are coming with less lot. Resale tends to be in more mature settings with better schools, access to shopping, and convivences.

Footnotes:

[1] National Association of Home Builders - https://www.nahb.org/news-and-economics/press-releases/2025/10/amid-market-challenges-builder-expectations-rise-in-october

[2] Freddie Mac - https://www.freddiemac.com/pmms/pmms_archives

[3] Federal Reserve - https://www.federalreserve.gov/newsevents/pressreleases/monetary20240918a.htm

[4] Federal Reserve - https://www.federalreserve.gov/aboutthefed/fedexplained/accessible-version.htm

[5] Census - https://w.census.gov/construction/nrs/pdf/newressales_202410.pdf

[6] Business Wire - https://www.businesswire.com/news/home/20251029552422/en/Redfin-Reports-27-of-For-Sale-Homes-Are-Newly-Built-the-Lowest-Share-in-4-Years

[7] Reuters - https://www.reuters.com/business/us-existing-home-sales-rise-seven-month-high-september-2025-10-23

[8] Wolf Street - https://wolfstreet.com/2025/09/24/inventory-of-new-completed-single-family-homes-jumps-to-highest-since-2009-but-sales-of-new-homes-see-outlier-spike-in-the-south-prices-skid-some-thoughts

[9] National Association of Home Builders - https://www.nahb.org/news-and-economics/press-releases/2025/10/amid-market-challenges-builder-expectations-rise-in-october

The “Double (Stuff) Contingency” on Construction Loans and How to Avoid It.

Custom contracts need a buffer…not a double-stuff. A contingency on top of a contingency is just way too much!

If you’re building a custom home you should carry a contingency. It’s smart risk management for the borrower, the builder, and the bank. A contingency is a buffer to the budget, and usually ranges from 5–10%, usually included in the total contract price. Creating a contingency is important as it provides flexibility to handle cost increases, change orders, and unknowns. The trouble starts when a lender layers on a second, or overlay contingency. That “double duty” silently inflates capital required to close, squeezes your appraisal, and can even knock your DTI out of bounds.

What goes wrong when the bank adds its own contingency

A) Your down payment requirement increases more than it should

Most lenders size the contingency in relation to the total cost o the contract. Since the pandemic, most builders work off a “cost plus” contract. This is perfectly acceptable, and adding a continency into the contract or having healthy reserves on the sideline insulates the deal accordingly. However, if a bank adds, say, a 10% overlay contingency on top of your contract’s 10% to accommodate a variable contact, your “cost” number balloons up which requires more money at closing to close.

For Example…

Let’s assume your base cost, not including the land is $900,000. Then add a 10% in-contract contingency for a total budget of $990,000.

Usually this is enough, but lately we have seen some lenders overlay and additional 10%. This increases the cost to $1,089,000 as the full “underwrite cost.”

If the loan is capped at 80% of cost, that extra $99k forces $79,200 more cash at closing for risk already addressed by the contract contingency.

B) Appraisal math gets tougher

Construction appraisals are completed “subject to completion per plans & specs” as finished today. Inflating the budget with a lender overlay doesn’t raise value, that is determined by the comps. As a result, the gap the appraisal needs to cover, which can push LTV higher than expected or force late stage budget surgery. Some lenders like to see 20% down and even more lenders like to use the lower of the appraised value or the total cost. Even if the bank has additional flexibility with the loan-to-value, it could force mortgage insurance, or a higher rate for the added risk.

C) Qualifying gets needlessly tight (DTI + taxes)

If the overlay swells the loan amount or the lender underwrites payments against a padded budget, your qualifying payment rises. With interest rates hanging in the 6 percent range, the round figure cost per $100,000 equates roughly to $600 per month. The next “X” factor is the estimated property taxes. That’s part of the danger of increasing the budget. Lenders have the habit of using a 1% property-tax placeholder for property taxes. It works well for states like Missouri, North Dakota, or Oklahoma. However, for Arizona, that could be another double whammy as Maricopa county often runs closer to 0.5%. Effectively, your DTI is penalized by assumptions, not reality.

The fix: keep the contingency where it belongs (while adding more flex)

Leverage a fixed-price contract with a defined 10% contingency inside the contract

That satisfies legitimate unknowns without inviting a second, lender buffer. It makes more sense to include it within the contract, stacking it on top is completely unnecessary.Offer documented capital reserves

If the lender wants extra comfort, present liquid reserves as the safety net. Reserves cover any tail risk without inflating loan amount, appraisal hurdles, or any potential increase on cash to close.Underwrite state-appropriate property taxes

The property taxes should be based on the property taxes from comparable sales. If the values is based on sales, so should the property taxes. Most counties offer data based on benchmarks determined by assessed value. 1% is still slim for a state like New Jersey and unrealistic for a state like Utah. Use the documented values instead of a blanket amount. Small change, big DTI difference.Partner with a lenders that offer “float-downs” for the perm loan

One of the principal advantages of a single close construction loan is the ability to lock in the rate at closing. Rates will be higher, lower, or the same when your home is ready for delivery. If there is a 30% chance rates may improve, partner with a lender that offers a free float down at loan conversion. Its a win for you and the lender saving you from an immediate refinance. The prospect of utilizing a float down is likely in a declining rate environment.

A simple, real-numbers walkthrough

Scenario A (single contingency):

Contract price (incl. 10% contingency): $990,000

Max loan: 80% of cost = $792,000

Cash to close (excluding land/fees): $198,000

Scenario B (double contingency):

Bank overlays +10% on top = “@” $1,089,000

Max loan 80% = $871,200

Extra cash required: +$79,200 vs. Scenario A

Exposes Appraisal, Qualifying Payment, Property Taxes, Reserves

That’s real money for “protection” you already had.

Why this matters right now

Yes, volatility is still in the air, but isn’t what it was a few years ago, so overcommitting to unknowns is harder to justify. Best practices include a heart to heart discussion with your builder and murphy’s law. If tariffs are a factor, find out ways to mitigate them and perhaps utilize a heathy draw at closing to lock in material costs. For some 10% may be just right, for others 6% should be perfect. The amount should come from you and your builder, not the lender. Every unnecessary dollar in a padded budget increases down payment and qualification stress without improving the results. Keep contingency precise & contract-based, not duplicated.

Checklist: how to keep your deal tight

Fixed-price or contract with appropriate contingency included.

Written lender acceptance, no separate bank overlay if adequate reserves are documented

Taxes underwritten using state benchmarks/county tools/appraisal comparables- not a 1% boilerplate

Partner with lender that offers single close loan, & free float down as rate insurance

Disclaimer: This is general education, not legal, tax, or credit advice. Program terms and eligibility can change. Always confirm specifics with your lender, builder, and tax adviser.